– Survey Shows a Majority of European Youth Would Participate in Uprising to Overthrow Status Quo:

As the title of today’s piece implies, something very rotten is happening across the Western world and it’s starting to push many people, especially the youth, toward a breaking point. In the U.S., much of the problem relates to increased corporate power and monopoly, which has resulted in a less dynamic economy characterized by a neo-feudal plantation model where a small group of people continue to rent-seek profits at the expense of society at large.

Surprisingly enough, today’s piece will zero in on the observations of fund manager Jeremy Grantham to make the point. In his quest to understand why P/E multiples and corporate profit margins have failed to revert to the prior mean over the past couple of decades, Mr. Grantham of GMO made some very important points about how the American economy has changed for the worse during the 21st century. Indeed, much of what he observes can be seen as key factors in rising income equality, which in turn leads to social instability.

Here are some of his key points from the latest GMO Quarterly Letter (it starts on page 9):

How about profit margins, the other input into the market level? Compared to the pre-1997 era, the margins have risen by about 30%. This is a large and sustained change.

Of all these many differences, the most important for understanding the stock market is, in my opinion, the much higher level of corporate profits. With higher margins, of course the market is going to sell at higher prices. So how permanent are these higher margins? I used to call pro t margins the most dependably mean-reverting series in nance. And they were through 1997. So why did they stop mean reverting around the old trend? Or alternatively, why did they appear to jump to a much higher trend level of pro ts? It is unreasonable to expect to return to the old price trends – however measured – as long as pro ts stay at these higher levels.

So, what will it take to get corporate margins down in the US? Not to a temporary low, but to a level where they uctuate, more or less permanently, around the earlier, lower average? Here are some of the influences on margins (in thinking about them, consider not only the possibilities for change back to the old conditions, but also the likely speed of such change):

– Increased globalization has no doubt increased the value of brands, and the US has much more than its fair share of both the old established brands of the Coca-Cola and J&J variety and the new ones like Apple, Amazon, and Facebook. Even much more modest domestic brands – wakeboard distributors would be a suitable example – have allowed for returns on required capital to handsomely improve by moving the capital- intensive production to China and retaining only the brand management in the US. Impeding global trade today would decrease the advantages that have accrued to US corporations, but we can readily agree that any setback would be slow and reluctant, capitalism being what it is, compared to the steady gains of the last 20 years (particularly noticeable after China joined the WTO).

– Steadily increasing corporate power over the last 40 years has been, I think it’s fair to say, the defining feature of the US government and politics in general. This has probably been a slight but growing negative for GDP growth and job creation, but has been good for corporate profit margins. And not evenly so, but skewed toward the larger and more politically savvy corporations. So that as new regulations proliferated,they tended to protect the large, established companies and hinder new entrants. Exhibit 5 shows the steady drop of net new entrants into the US business world – they have plummeted since 1970! Increased regulations cost all corporations money, but the very large can better a afford to deal with them. Thus regulations, however necessary to the well-being of ordinary people, are in aggregate anti-competitive. They form a protective moat for large, established firms. This produces the irony that the current ripping out of regulations willy-nilly will of course reduce short-term corporate costs and increase profits in the near future (other things being equal), but for the longer run, the corporate establishment’s enthusiasm for less regulation is misguided: Stripping out regulations is working to fill in its protective moat.

– Corporate power, however, really hinges on other things, especially the ease with which money can influence policy. In this, management was blessed by the Supreme Court, whose majority in the Citizens United decision put the seal of approval on corporate privilege and power over ordinary people. Maybe corporate power will weaken one day if it stimulates a broad pushback from the general public as Schumpeter predicted. But will it be quick enough to drag corporate margins back toward normal in the next 10 or 15 years? I suggest you don’t hold your breath.

– It is hard to know if the lack of action from the Justice Department is related to the increased political power of corporations, but its increased inertia is clearly evident. There seems to be no reason to expect this to change in a hurry.

– Previously, margins in what appeared to be very healthy economies were competed down to a remarkably stable return – economists used to be amazed by this stability – driven by waves of capital spending just as industry peak profits appeared. But now in a very different world to that described in Part 1,4 there is plenty of excess capacity and a reduced emphasis on growth relative to profitability. Consequently, there has been a slight decline in capital spending as a percentage of GDP. No speedy joy to be expected here.

– The general pattern described so far is entirely compatible with increased monopoly power for US corporations. Put this way, if they had materially more monopoly power, we would expect to see exactly what we do see: higher profit margins; increased reluctance to expand capacity; slight reductions in GDP growth and productivity; pressure on wages, unions, and labor negotiations; and fewer new entrants into the corporate world and a declining number of increasingly large corporations. And because these factors a ect the US more than other developed countries, US margins should be higher than theirs. It is a global system and we out-brand them for one thing.

– The single largest input to higher margins, though, is likely to be the existence of much lower real interest rates since 1997 combined with higher leverage. Pre-1997 real rates averaged 200 bps higher than now and leverage was 25% lower. At the old average rate and leverage, profit margins on the S&P 500 would drop back 80% of the way to their previous much lower pre-1997 average, leaving them a mere 6% higher. (Turning up the rate dial just another 0.5% with a further modest reduction in leverage would push them to complete the round trip back to the old normal.)

What I found most interesting about the above observations is that they weren’t the ramblings of a political stooge trying to get elected for something, but rather the sincere conclusions of an investment manager trying to figure out why profit margins aren’t reverting to the mean. In doing so, he provided us with some very valuable nuggets about the underlying sickness of the U.S. economy, and why elevated corporate profits is a sign of economic weakness, not strength.

I actually wrote about this exact topic all the way back in 2012 in the piece, The Stock Market: Food Stamps for the 1%. Here’s some of what I observed at the time:

More than any other group, the 1% has been convinced that the stock market represents some sort of leading indicator of wealth and prosperity. Nothing could be further from the truth. Sure, the stock market can function as such an indicator. It is such an indicator when the rising stock market reflects a dynamic, capitalist economy where new industries and companies are rising to the top and improving standards of living for the populace. It represents the opposite indicator when it merely reflects the ownership interests of the oligarchs in a crony-capitalist, fascist economy that is picking away at the dying carcass of what little economic freedom still remains. This is what a rising stock market actually represents today. When people look at it they should understand it is merely a measure of the oligarchs getting wealthier and more powerful and you becoming more of a debt slave. It represents their interests in multinational corporations with record profit margins because they refuse to pay their employees a living wage. A rising stock market today is actually a leading indicator of the destruction of the middle class, cultural destitution and a society in collapse.

The stock market is like slop in a pigpen. It is a key instrument used to keep the 1% from getting antsy. Unlike the middle class (a group that isn’t falling for any of the tricks), many of the 1% work on Wall Street or related industries and own stocks. Many of the people in the 1% are at least wealthy and connected enough to still cause serious problems for the oligarchs. They must be kept quiet as the coup that started in 2008 is brought to fruition. Then they will be left high and dry like everyone else. This is the role that the stock market is playing at the moment.

So as the 1% sits around analyzing a casino, the poor collect food stamps and the middle class dies. Many in the 1% look upon the poor on food stamps with disdain, yet little do they realize they are on food stamps as well. It’s called the stock market.

Moving back to Grantham, he goes on to write the following:

Income inequality that may be helping to keep growth and rates lower will, unfortunately, in my opinion, also take decades to move materially unless we have a very unexpected near revolution in politics.

Here’s where I disagree with his forecast. The revolution in politics he accurately thinks it will take to change things is very much here, and will become far more noticeable in the years to come. I think Grantham is looking at Trump “populism” and concluding that his policies are largely very corporate profit margin friendly. I agree with this assessment, which is why I see Trump as a fake populist. That said, there’s another ascendant populist movement happening on the other side of the ideological spectrum, and I expect it to take hold as the preeminent U.S. political force going forward.

The likely catalyst for this alternative populist vision to take hold will be a failure of Trumpisms to help average Americans improve their everyday lives. Although progressive populism is still somewhat nascent, it is quite popular amongst the youth, and will likely become increasingly so as issues of student debt and healthcare costs begin to dominate the conversation far more than they do today. The Bernie Sanders movement was merely a tremor in a much larger earthquake likely to sweep across the land in the years ahead.

This sort of movement is precisely the sort which will cause the type of “revolution in politics” Mr. Grantham considers unexpected. Not only do I expect it, I think it might be much closer to affecting policy than he thinks (I think 2020-2030 could be dominated by this sort of politics).

Moving along to the title of this post, disillusionment and despair are even father along the spectrum in parts of Europe than in the U.S., which can be evidenced by the following excerpts from Quartz:

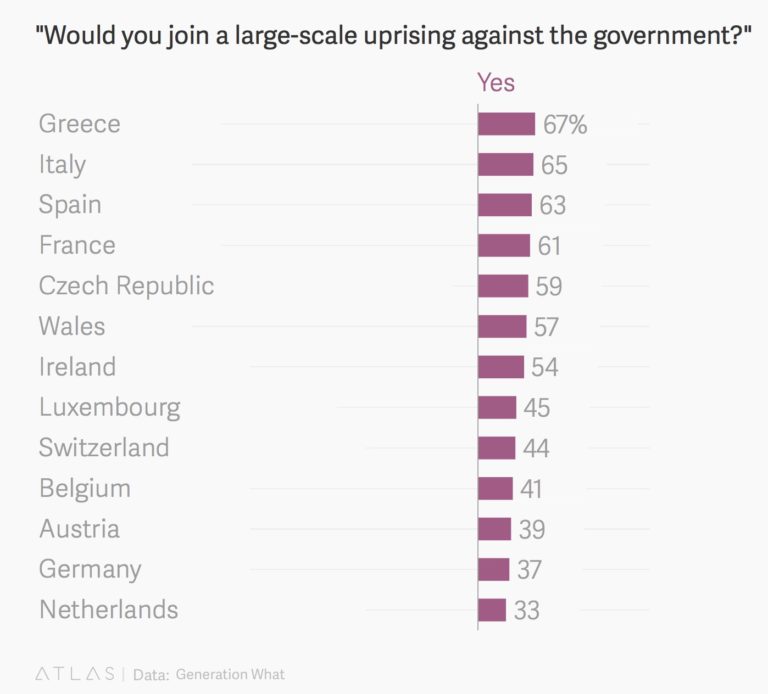

Around 580,000 respondents in 35 countries were asked the question: Would you actively participate in large-scale uprising against the generation in power if it happened in the next days or months? More than half of 18- to 34-year-olds said yes.

The question was part of a European Union-sponsored survey, titled “Generation What?” The report went on to focus on respondents from 13 countries to better understand what young people are optimistic and frustrated about in Europe. Among these spotlighted countries, young people in Greece were particularly interested in joining a large-scale uprising against their government, with 67% answering yes to the question. Respondents in Greece were also more likely to believe politicians were corrupt and to have negative perceptions of the country’s financial sector.

While some observers are hoping that the defeat of Gert Wilders in the Netherlands and the expected loss of Le Pen in France will herald the beginning of the end for populist momentum in the Western world, I have bad news for you. Not only will populism stay ascendant, we are merely in the very early stages of this ongoing political earthquake. I do not expect this trend to go away until the economic future for average citizens (especially the youth) starts to improve materially.

If you enjoyed this post, and want to contribute to genuine, independent media, consider visiting our Support Page.

In Liberty,

Michael Krieger

* * *

PayPal: Donate in USD

PayPal: Donate in EUR

PayPal: Donate in GBP