– Asia Crashes, Europe Slides, US Rebounds But Yields Resume Ominous Rise

* * *

PayPal: Donate in USD

PayPal: Donate in EUR

PayPal: Donate in GBP

The man who trades freedom for security does not deserve nor will he ever receive either. – Benjamin Franklin

– Dow Jones – 100 Year Historical Chart

H/t reader kevin a:

“This site has very nice free charts”

* * *

PayPal: Donate in USD

PayPal: Donate in EUR

PayPal: Donate in GBP

– White House Issues Statement On Today’s Historic Market Crash:

Today, the Dow Jones suffered (including the plunge after hours) its biggest point crash in history, turning negative for the year, which for a president who takes particular delight in every uptick in the market, was terrible news.

So, as many expected, the White House issued a statement after the close, commenting on today’s market crash.

Predictably, there was little commentary of the “day to day” moves, and instead Trump deflected by pointing out that he is now focusing on the economy’s “long-term fundamentals” instead.

Full statement below:

“The President’s focus is on our long-term economic fundamentals, which remain exceptionally strong, with strengthening U.S. economic growth, historically low unemployment, and increasing wages for American workers. The President’s tax cuts and regulatory reforms will further enhance the U.S. economy and continue to increase prosperity for the American people.

Translation: Trump will never again tweet about the market.

* * *

PayPal: Donate in USD

PayPal: Donate in EUR

PayPal: Donate in GBP

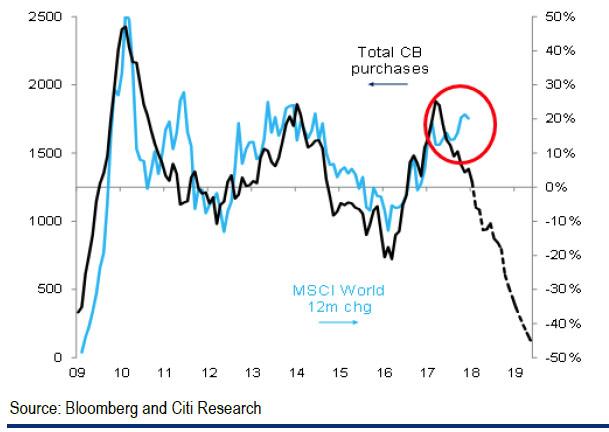

According to Citi, by mid-2019, equities are facing a nearly 50% drop to keep pace with the upcoming central bank asset shrinkage.

– Bonds Finally Noticed What Is Going On… Stocks Are Next

* * *

PayPal: Donate in USD

PayPal: Donate in EUR

PayPal: Donate in GBP

– This Could Be The Hottest Mining Stock Of 2018:

In the forests of Colombia, a record-breaking discovery was made.

A 1759-carat emerald was uncovered from the Coscuez mine. It is now part of the collection of the Banco Nazionale of Columbia. The massive jewel could be worth as much as $17 million, based on current per-carat estimates.

…

H/t reader kevin a.

* * *

PayPal: Donate in USD

PayPal: Donate in EUR

PayPal: Donate in GBP

– The 2018 Stock Market Bubble vs. Gold & Silver:

The U.S. Stock Market is reaching its biggest bubble in history. When the price of the Dow Jones Index only moves in one direction… UP, it is setting up for one heck of a crash. While market corrections aren’t fun for investors’ portfolios, they are NECESSARY. However, it seems that corrections are no longer allowed to take place because if they did, then the tremendous leverage in the market might turn a normal correction into panic selling and a meltdown on the exchanges.

So, we continue to see the Dow Jones Index hit new record highs, as it moved up 765 points since the beginning of the year. Now, if w go back to 1981 when the Dow was trading about 800 points, it took five years to double itself by another 800 points. However, the Dow Jones Index just added 765 points in less than two weeks. It doesn’t matter if the (1) point increase in the Dow Jones today is insignificant compared to a (1) point increase in 1981, investors feel rich when the numbers are increasing in a BIG WAY.

With one name change, we can now confirm that the efficient market hypothesis is dead and buried.

– Long Blockchain Sells 1.6 Million Shares, Will Buy 1,000 Bitcoin Mining Machines:

The “blockchain” farce is now complete.

…

* * *

PayPal: Donate in USD

PayPal: Donate in EUR

PayPal: Donate in GBP

– I’m in Awe of How Far the Scams & Stupidities around “Blockchain Stocks” are Going:

It just doesn’t let up. UBI Blockchain Internet, a Hong Kong outfit whose shares trade in the US [UBIA], filed with the SEC to sell an additional 72.3 million shares owned by its executives. In other words, it isn’t selling the shares to raise money for corporate purposes, but to allow its executives, including CEO Tony Liu, to bail out.

This is happening after the company – which sports zero revenues and a disconnected phone number in its SEC filings – managed to get its shares to spike briefly by over 1,100%, pushing its market capitalization to $8 billion.

Read moreI’m in Awe of How Far the Scams & Stupidities around “Blockchain Stocks” are Going

– 2017 Has Been The Best Year For The Stock Market EVER:

We have never seen a better year for stocks in all of U.S. history. Just five days after Donald Trump entered the White House, the Dow Jones Industrial Average hit the 20,000 mark for the first time ever. On Monday, the Dow closed at 24,792.20, and there doesn’t seem to be any end to the rally in sight. Overall, the Dow Jones Industrial Average is up more than 5,000 points so far in 2017, and that absolutely shatters all of the old records. Previously, the most that the Dow had risen in a single year was 3,472 points in 2013.

Yes, I know that it may seem odd for a website that continually chronicles our ongoing “economic collapse” to be talking about a boom in stock market prices. But of course there has not been a corresponding economic boom to match the rise in stock prices. This artificial stock market bubble has been created by unprecedented central bank intervention, and every previous stock market bubble in our history has ended with a horrible crash.

Read more2017 Has Been The Best Year For The Stock Market EVER

FYI.

https://youtu.be/ynmwL8NeXoA

– Peter Schiff Warns Of “Too Big To Pop” Bubble – “Everybody Is Going To Get Wiped Out!”:

Money manager Peter Schiff correctly predicted the financial meltdown in 2008.

Now, 10 years later, what does Schiff see today? Schiff says,

“I predicted a lot more than just the stock market going down back then. I predicted the financial crisis, but more importantly, I predicted what the government would do as a result of the financial crisis and what the consequences of that would be because that’s where we’re headed.

The real crash I wrote about in my most recent book is still coming…

Read morePeter Schiff Warns Of “Too Big To Pop” Bubble – “Everybody Is Going To Get Wiped Out!”

– The Corporate Earnings Fiction in Q3:

All 30 companies in the Dow Jones Industrial Average have now reported earnings for the third quarter. As required, they reported these earnings under Generally Accepted Accounting Principles (GAAP). These standardized accounting rules are supposed to allow investors to compare the results of different companies. But that’s too harsh a fate for many of our corporate heroes, and so they proffer their own and much more pleasing accounting strategies – as expressed in “adjusted” earnings and “adjusted” earnings per share (EPS).

Of the 30 companies in the DJIA, 14 reported “adjusted” or “non-GAAP” earnings in Q3 that were significantly higher than their GAAP earnings. Total “adjusted” EPS of these 14 Dow components exceeded their total EPS under GAAP by 26%! Nice work!