It’s the question investors everywhere are wrestling with: Are asset prices in a bubble, or do they simply reflect the fact that the global economy is growing once again?

For Marc Faber, editor of the Gloom, Boom & Doom Report, the answer is clear. In fact, he says the bubble may already be bursting.

“I think it’s a colossal bubble in all asset prices, and eventually it will burst, and maybe it has begun to burst already,” Faber said Tuesday on CNBC’s ‘Futures Now’ as the S&P 500 lost ground for the second-straight session.

More of the same from Janet Yellen in her latest speech, but her focus on “resilience” caught my attention as it relates to very recent developments. The taper threat experience last year may have been a warning, but it doesn’t seem like it resonated with her or policymakers. The major bond selloff, which led to global ripples of crisis in credit, funding and currencies, was the opposite of flexibility. Perhaps a better definition of the word would be a place to start.

But her meaning was a bit different, in that it is clear (from this speech and prior assertions, wrong as they were, about the mid-2000’s housing bubble) she sees bubbles as “market” events in which the central bank’s role is primarily shock absorption. In other words, idiot investors wholly of their own accord create bubbles and it’s the job of the munificent and enlightened Federal Reserve to help ensure that such “market” madness is “contained” without further economic destruction.

While the growth of China’s ghost cities of entirely derelict and unlived-in residential real estate have become anathema; the story of the nation’s ‘if we build it they will come’ commercial real estate bubble has been less exposed but is no less incredible. As Bloomberg reports, China’s project to build a replica Manhattan is taking shape against a backdrop of vacant office towers and unfinished hotels, underscoring the risks to a slowing economy from the nation’s unprecedented investment boom. Stunningly, the development has failed to attract tenants since the first building was finished in 2010 leaving one commercial real estate investor to proclaim, “Investing here won’t be better than throwing money into the water… There will be no way out – it will be very difficult to find the next buyer.”

China’s own Big Apple may be rotting from the core. A new central business district modeled after New York City is going up in Tianjin…but the nation’s slowing economy is exacerbating the risks from its unprecedented credit binge…and that’s putting China’s Manhattan project in jeopardy. Bloomberg TV’s China Correspondent Stephen Engle reports.

While US central bankers shudder at the idea of admitting their could be a bubble in real estate or stocks (unless its obvious in hindsight); and England’s Bank of England explains ‘if there is a bubble, it’s not their fault, but there isn’t so there’; it appears the Chinese are more comfortable with the truth. As Bloomberg BusinessWeek reports, China’s central bank Governor Zhou Xiaochuan said, China may have a housing bubble only in “some cities,” – an issue that’s difficult to resolve with a single nationwide policy. As concerns mount of dramatic over-supply on the back of extrapolated urbanization dreams, Zhou notes, “The economy has slowed down a bit, but not very much,” adding that “we should keep vigilance on whether it continues to slow down.” Which is odd because US talking heads have made up their minds that China is fixed…

We have covered the topic of the student loan bubble extensively in the past so we won’t waste more digital ink on where it comes from or what it means for the troubled US consumer, suffice to report that according to the Fed, in Q1 total Federal student loans rose by another $31 billion to a record $1.11 trillion, and up a whopping $125 billion, or 12% from this time last year.

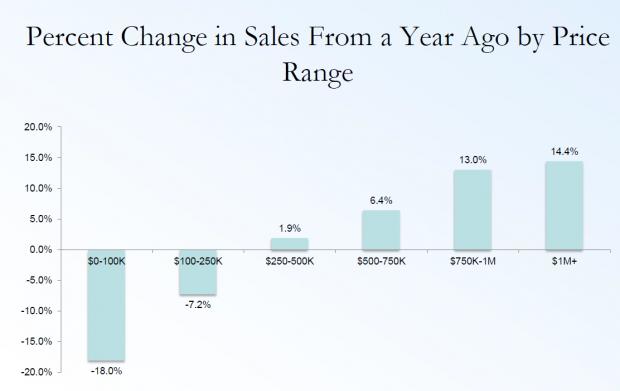

While the housing bubble for anything but the ultra luxury segment has long since popped with $1.1 trillion of student loans playing a significant role in the burst, (as explained in “Stick A Fork In The “Housing Recovery“), as can be seen in the chart below which shows that the only increase in existing home sales from a year ago is that for the $500 and over price range (which accounts for only 10% of all actual transactions)….

… when it comes to the luxury segment, things have moved beyond the simply bizarre and have entered outright surreal territory.

When it comes to real estate, we know that Californians enjoy drinking from the gold cup of mania. Lusting over real estate seems to be as common as traffic on the 405. People in California have a deep rooted cultural and economic amnesia. I bet half the population has very little idea regarding the history of many cities in Southern California. Heck, most don’t even know where their drinking water comes from. So trying to discuss Fed policy, skewing based on investors, or market manipulation with a large portion of people is like talking to your dog about Hemmingway. Some people only understand “real estate goes up!” and when it doesn’t, they only understand “buying is bad!” California real estate is overvalued by most economic measures. Sure, people are willing to pay insane prices but they did this as well in 2006 and 2007 and people also paid crazy prices for tech companies in a previous delusion based boom. Investors are pulling back because they simply don’t perceive value at current prices. We are now seeing more reports putting a price on how overvalued the region is. Fitch Ratings and Trulia both point to SoCal as being massively overpriced. In fact, Fitch Ratings has Orange County overvalued by a whopping 30 percent. Congratulations to Orange County for being the most overpriced county in the entire United States.

Since the bursting of the first US housing bubble in 2007, one of the primary explicit goals of the Fed has been to reflate the very same housing bubble (whose pop, together with the credit bubble, nearly wiped out the western financial system) as housing, far more than stocks, is instrumental to the “wealth effect” of the broader population (as opposed to just the 1%).

Sadly for the Fed, instead of recovering previous highs, median housing prices (not to be confused with the ultraluxury high end where prices have never been higher) have stagnated and are now in the downward phase of the fourth consecutive dead cat bounce, curiously matching a like amount of Fed monetary injection episodes.

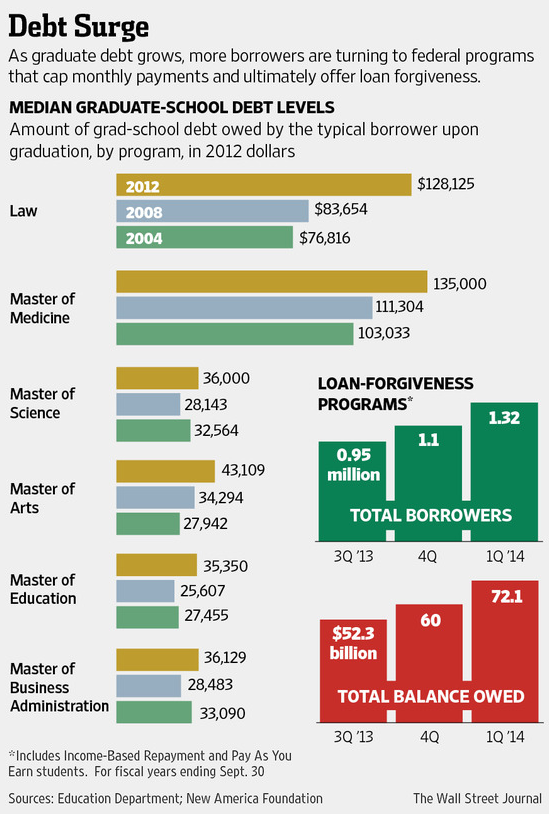

“Loan forgiveness creates incentives for students to borrow too much to attend college, potentially contributing to rising college prices for everyone,” is a study’s warning over government plans that allow students to rack up big debts and then forgive the unpaid balance after a set period. As WSJ reports, enrollment in student debt forgiveness plans have surged nearly 40% in just six months, to include at least 1.3 million Americans owing around $72 billion. The administration is looking to cap debt eligible for forgiveness, as President Obama’s revamped Pay As You Earn scheme has seen applications soar and is estimated to cost taxpayers $14bn a year. The ‘popularity’ of the student loan bailout plan surged after Obama promoted it in 2012, and now the administration must back-track as costs have massively outpaced government predictions.

We have been aggresively focused on the government’s blowing of the student loan bubble…

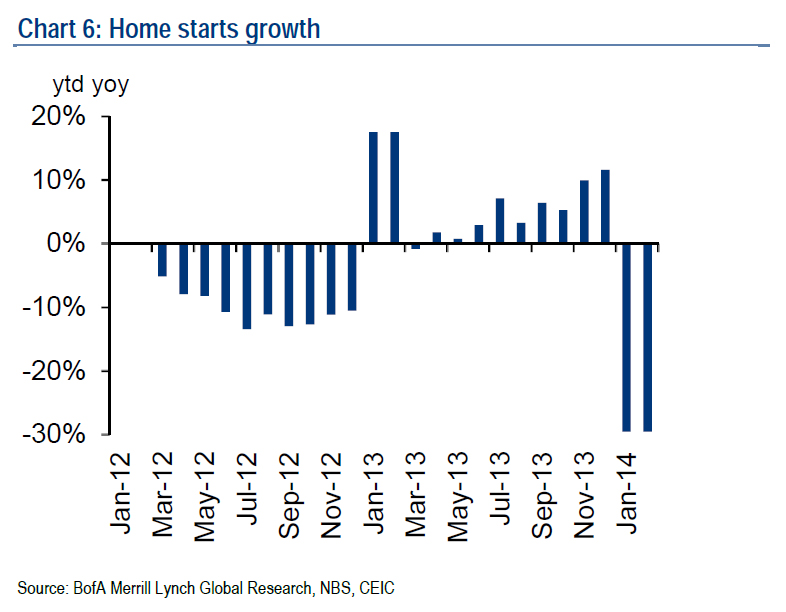

The one problem with every Ponzi scheme is that it must constantly grow, in both demand and supply terms, for the mass delusion to continue. The other problem, of course, is that every Ponzi scheme always comes to an end…. which may have just happened in China where as the chart below shows, as of this moment at least, the supply side to the Chinese housing ponzi (and recall that in China the bubble is not in the stock market like in the US, but in housing) has slammed shut.

None of the problems that caused the last financial crisis have been fixed. In fact, they have all gotten worse. The total amount of debt in the world has grown by more than 40 percent since 2007, the too big to fail banks have gotten 37 percent larger, and the colossal derivatives bubble has spiraled so far out of control that the only thing left to do is to watch the spectacular crash landing that is inevitably coming. Unfortunately, most people do not know the information that I am about to share with you in this article. Most people just assume that the politicians and the central banks have fixed the issues that caused the last great financial crisis. But the truth is that we are in far worse shape than we were back then. When this financial bubble finally bursts, the devastation that we will witness is likely to be absolutely catastrophic.

American students are well over $1 trillion in debt, and it’s starting to hurt everyone, economists say

Chris Rong did everything right. A 23-year-old dentistry student in New York, Chris excelled at one of the country’s top high schools, breezed through college, and is now studying dentistry at one of the best dental schools in the nation.

But it may be a long time before he sees any rewards. He’s moved back home with his parents in Bayside, Queens—an hour-and-a-half commute each way to class at the New York University’s College of Dentistry—and by the time he graduates in 2016, he’ll face $400,000 in student loans. “If the money weren’t a problem I would live on my own,” says Rong. “My debt is hanging over my mind. I’m taking that all on myself.”

China is now the second largest economy in the world and for the last 30 years China’s economy has been growing at an astonishing rate, wowing the world, as spending and investment has been undertaken on a scale never seen before in human history – 30 new airports, 26,000 miles of motorways and a new skyscraper every five days have been built in China in the last five years. But as we (and Michael Pettis, George Soros, and Jim Chanos – among many others) have warned, it is all eerily reminiscent of what happened in the West… the vast majority of it has been built on credit. This has now left the Chinese economy with huge debts and questions over whether much of the money can ever be paid back (spoiler alert: it can’t and it won’t).

The BBC’s Robert Peston travels to China to investigate how this mighty economic giant could actually be in serious trouble.

Did you know that financial institutions all over the world are warning that we could see a “mega default” on a very prominent high-yield investment product in China on January 31st? We are being told that this could lead to a cascading collapse of the shadow banking system in China which could potentially result in “sky-high interest rates” and “a precipitous plunge in credit“. In other words, it could be a “Lehman Brothers moment” for Asia. And since the global financial system is more interconnected today than ever before, that would be very bad news for the United States as well. Since Lehman Brothers collapsed in 2008, the level of private domestic credit in China has risen from $9 trillion to an astounding $23 trillion. That is an increase of $14 trillion in just a little bit more than 5 years. Much of that “hot money” has flowed into stocks, bonds and real estate in the United States. So what do you think is going to happen when that bubble collapses?

One of the men that won the Nobel Prize for economics this year says that “bubbles look like this” and that he is “most worried about the boom in the U.S. stock market.” But you don’t have to be a Nobel Prize winner to see what is happening. It should be glaringly apparent to anyone with half a brain. The financial markets have been soaring while the overall economy has been stagnating. Reckless injections of liquidity into the financial system by the Federal Reserve have pumped up stock prices to ridiculous extremes, and people are becoming concerned. In fact, Google searches for the term “stock bubble” are now at the highest level that we have seen since November 2007. Despite assurances from the mainstream media and the Federal Reserve that everything is just fine, many Americans are beginning to realize that we have seen this movie before. We saw it during the dotcom bubble, and we saw it during the lead up to the horrible financial crisis of 2008. So precisely when will the bubble burst this time? Nobody knows for sure, but without a doubt this irrational financial bubble will burst at some point.

Remember, a bubble is always the biggest right before it bursts, and the following are 15 signs that we are near the peak of an absolutely massive stock market bubble:

The maestro clarifies his ‘experienced’ perspective of spotting bubbles in the following quote from his interview with Bloomberg TV’s Al Hunt:

“This does not have the characteristics, as far as I’m concerned, of a stock market bubble,”

Of course, as we noted here, some would beg to differ; but perhaps what would be useful is for the former Fed head to explain what ‘characteristics’ do constitute a bubble…

Most people – certainly most governments and economists – define inflation as a general rise in prices. But this is wrong. Inflation is an increase in the money supply, of which a rising general price level is just one possible result – and not the most common one.

More often, excessive money creation shows up as asset bubbles, where the new money, instead of flowing equally to all the products that are for sale at a given time, flow disproportionately into the ‘hottest’ asset classes. Readers who were paying attention in the 1990s might recall that the consumer price index was well-behaved while huge amounts of money flowed into financial assets, producing the dot-com bubble.

The same thing happened in the 2000s, when excess currency flowed into housing and equities. In each case, mainstream economists and government officials pointed to modest consumer price inflation as a sign that things were fine. And in each case they were simply looking in the wrong place and completely missing the destabilizing effects of an inflating money supply.

“The question is not ‘tapering’,” Marc Faber exclaims to his hosts on CNBC’s Squawk Box this morning, “the question is at what point will they increase the asset purchases to say $150 [billion] , $200 [billion], or a trillion dollars a month.” QE-4-EVA is here to stay, as Faber explained “every government program that is introduced under urgency and as a temporary measure is always permanent.” Simply put, “The Fed has boxed itself into a position where there is no exit strategy,” and while inflation may not be present in the ‘chosen’ indicators, Faber blasts, there’s been incredible asset inflation – “we are the bubble. We have a colossal asset bubble in the world [and] a leverage or a debt bubble.” There will be massive wealth destruction, he concludes, “one day this asset inflation will lead to a deflationary collapse one way or the other. We don’t know yet what will cause it.”

The Fed is Boxed In….

The world is in a gigantic bubble…

Back in April 2012, Faber saidthe world will face “massive wealth destruction” in which “well to-do people will lose up to 50 percent of their total wealth.”

In today’s “Squawk” appearance, he said that could still happen but possibly from higher levels because of the “asset bubble” caused by the Fed.

Almost exactly one year ago we wrote “The Next Subprime Crisis Is Here: Over $120 Billion In Federal Student Loans In Default” in which we took the latest (2009 three year cohort) loan default data on Federal Student Loans released by the Department of Education and applied it to the total amount of student loans outstanding, which back then was $914 billion. Yesterday, ED.gov provided its annual update – this time to the 2010 three year and 2011 two year cohorts – and to nobody’s major surprise, learned that things just got even worse. To wit: “The national two-year cohort default rate rose from 9.1 percent for FY 2010 to 10 percent for FY 2011. The three-year cohort default rate rose from 13.4 percent for FY 2009 to 14.7 percent for FY 2010.” Putting this in context, according to Bloombergdefaults have risen to the highest level since 1995. The irony that this is happening in the aftermath of Bernanke’s disastrous ZIRP policy is not lost on anyone.

Quantifying this percentage, recall the NY Fed reported in its second quarter household credit update that the amount of total outstanding student loans has now risen to $994 billion, or $80 billion more in just one year:

… one can calculate that the current amount of non-performing loans originated in 2010 is now a whopping $146 billion (the full total amount of student loans owed is $1.2 trillion when including private loans from the likes of Sallie Mae – this sum surpasses all other kinds of consumer borrowing expect for mortgages). Unfortunately, as the economic situation has only deteriorated since then especially for student-age Americans, the real blended amount of student loans in default is almost certainly substantially higher as of this moment.

If the Fed was worried about ‘froth’ in the markets earlier in the year, then this chart should have them panicking. Of course, as Jim Bullard noted Friday, there is no bubble because everyone knows there is no bubble but judging by the massive surge in covenant-lite loan issuance, there is a bubble in forced demand for leveraged loans. At $188.7 billion, the 2013 issuance of these highly unsafe loans (which have seen huge inflows since the Fed started talking taper back in May) is almost double that of the peak of the last credit bubble in 2007 and is five times the size of 2012 YTD issuance at this time. As Reuters notes, Covenant-lite loans used to be reserved for stronger companies and credits, but are now so common in the U.S. leveraged loan market that investors are becoming wary of some credits with a full covenant package. With corporate leverage at all-time highs, what could go wrong?

If you have a job that involves building homes, buying homes, selling homes or that is in any way related to the mortgage industry, you might want to start searching for alternate employment. Seriously. Interest rates are starting to rise dramatically, and mortgage lenders such as Bank of America, Wells Fargo and JPMorgan Chase are all cutting thousands of mortgage-related jobs. Last week, mortgage refinance activity plunged to the lowest level that we have seen since June 2009 and total mortgage activity dropped to the lowest level since October 2008. Unfortunately, this is only the beginning. Mortgage rates closely mirror the yield on 10 year U.S. Treasuries, the the yield on 10 year U.S. Treasuries has nearly doubled since early May. But it is still only sitting at about 3 percent right now. As I have written about previously, it has a ton of room to go up before it hits “normal” historical levels, and so do mortgage rates. As I noted the other day, some analysts believe that the yield on 10 year U.S. Treasuries is going to hit 7 percent eventually. If that happens, mortgage rates will be more than double what they are today. And we have already seen the average rate on a 30 year fixed rate mortgage go from 3.35 percent in May to 4.57 percent last week. If interest rates continue to rise we could be heading for a “housing Armageddon” that will make the last housing crash look like a Sunday picnic.

In August 2012, when isolating one of the various reasons for the latest housing bubble, we suggested that a primary catalyst for the price surge in the ultra-luxury housing segment and the seemingly endless supply of “all cash” buyers (standing at an unprecedented 60% of all buyers lately as reported by Goldman) is a very simple one: crime. Or rather, the use of US real estate as a means to launder illegal offshore-procured money. We also identified the one key permissive feature which allowed this: the National Association of Realtors’ exemption from Anti-Money Laundering provisions. In other words, all a foreign oligarch – who may or may not have used chemical weapons in their past: all depends on how recently they took their picture with the Secretary of State – had to do to buy a $47 million Florida house, was to get the actual cash to the US. Well good thing there are private jets whose cargo is never checked.

And the bid hits just keep on coming.While previously we reported the foreigners as an aggregate class sold the most gross US securities ever in the month of June, we also learned that in June the biggest selling came from America’s two largest creditors: China and Japan (excluding the Fed of course, whose P&L losses are now approaching $300 billion in the past 3 months, or would if the Fed marked to anything but unicorns).

In June, the two countries combined sold $42 billion, with each selling over $20 billion: the most in years.

What is interesting is looking at the composition of the selloff: the bulk of was in the form of short-term Bills, as both countries were actually buyers of coupon securities. Net of coupon purchases Bill sales were even worse, or over $50 billion for the two countries alone.

Will rapidly rising interest rates rip through the U.S. financial system like a giant lawnmower blade? Yes, the U.S. economy survived much higher interest rates in the past, but at that time there were not hundreds of trillions of dollars worth of interest rate derivatives hanging over our financial system like a Sword of Damocles. This is something that I have been talking about for quite some time, and now a Mexican billionaire has come forward with a similar warning. Hugo Salinas Price was the founder of the Elektra retail chain down in Mexico, and he is extremely concerned that rising interest rates could burst the derivatives bubble and cause “massive bankruptcies around the globe”. Of course there are a whole lot of people out there that would be quite glad to see the “too big to fail” banks go bankrupt, but the truth is that if they go down our entire economy will go down with them. Our situation is similar to a patient with a very advanced stage of cancer. You can try to kill the cancer with drugs, but you will almost certainly kill the patient at the same time. Well, that is essentially what our relationship with the big banks is like. Our entire economic system is based on credit, and just like we saw back in 2008, if the big banks start failing credit freezes up and suddenly nobody can get any money for anything. When the next great credit crunch comes, every important number in our economy will rapidly start getting much worse.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More https://infiniteunknown.net/dsgvo/

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

{kind=link}

{kind=link}