– Ukraine Enters The Endgame (ZeroHedge, Feb 25, 2015):

Back in March 2014 we forecast that it in the aftermath of the US State Department-sponsored military coup in Kiev, it was only a matter of time before Ukraine (all of its sovereign gold having since “vaporized“) succumbed to full blown hyperinflation and economic implosion. Less than a year later, precisely this outcome has finally played out, and as a result, the entire nation has finally entered its economic endgame, one which has two conclusion: either it joins Greece in becoming a ward of Europe (of which it is not an official member) and the IMF (thank you Joe Q Public taxpayer), or it quietly fades away into insolvent “failed state” status.

This is in a nutshell the assessment by Goldman Sachs, presented below, which really doesn’t say much we didn’t cover earlier in “Ukraine Enters Hyperinflation: Currency Trading Halted, “Soon We Will Walk Around With Suitcases For Cash“, but which does lays out the (very unpleasant) alternatives for yet another nation brought to ruin through American neo-colonial expansion, in what may well be a record short period of time. Of these, the primary ones focus on yet another IMF bailout which the agency may find some resistance to as a result of the near-total collapse of Greece at the same time. And not only that but Goldman’s “base case of IMF fund disbursement in mid-March may not come quickly enough to stabilize the Hryvnia.” Oops.

Should the IMF fail to provide the much needed funding (and as of this moment the days of merely jawboning its support for the central banks are finished since Russia will once again shut down its gas to Kiev unless it is paid in full and upfront), this is what happens: “the Ukrainian authorities could tighten FX controls further. In the extreme, this could potentially involve a bank deposit freeze, a ban on retail FX purchases and/or moratorium on external payments and complete closure of the capital account.”

Hence our question to Ukrainians: was the coup worth the economic disintegration of your nation, and leaving your faith in the hands of the US, whose recent global intervention case-studies include such sterling examples as Libya, Egypt and Iraq?

And before we present the Goldman piece, here is something truly funny: in discussing the causes of the collapse of the Ukraine currency, Goldman lays out “monetary financing of Ukraine’s fiscal deficits” as one of the reasons.

This is certainly not funny for Ukraine which now may have just enough cash to cover 3 weeks worth of imprts:

While monetary financing of the deficit may debase the value of the Hryvnia in the medium term, it is the shortage of FX in the system that has caused the proximate pressure on the currency, as NBU reserves declined to US$6.4bn in January (4 weeks of imports) and are likely to decline to US$5-5.5bn in February (3 weeks of import cover). These international reserves include about US$1bn in monetary gold, so the liquid amount of reserves is likely to fall to US$4-4.5bn in February (2.5 weeks of imports).

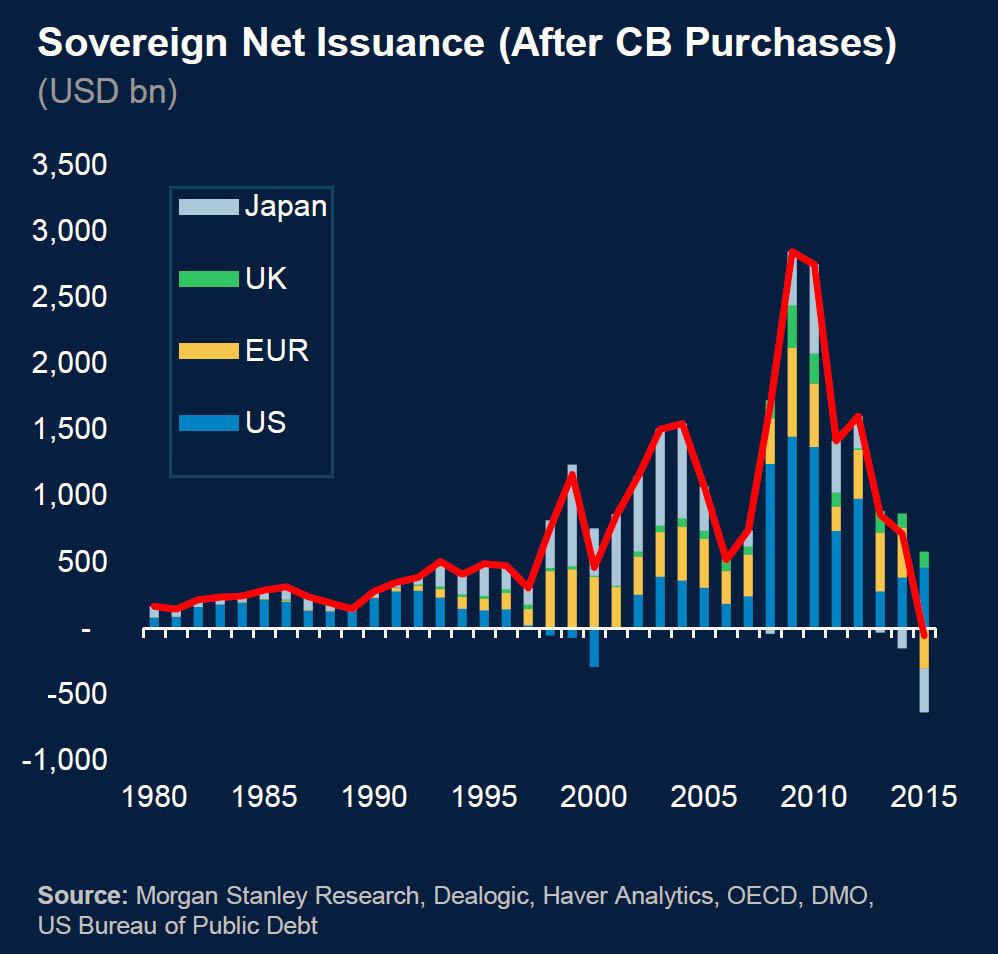

So why is it that funny? Because as the chart below shows, it is not just Ukraine that is engaged in “monetary financing of its deficit” – so is the entire developed world to the point where central banks will buy up every single dollar of debt government have to issue (and thus fund deficits) and then some!

In other words, we now live in a world in which the entire global fiscal, and every other, debt-funded deficit is being plugged by central banks! Therefore, for anyone curious what will eventually happen to the world’s various fiat currencies, look no further than the UAH.

So without further ado, here is Goldman with “As pressure builds on the Hryvnia, short-term risks mount and may prompt policy action”

Bottom line:

The Hryvnia weakened over the weekend to UAH 30 vs. the USD, prompting the Ukrainian authorities to tighten FX controls and to intervene by a reported US$80mn today, and causing a further weakening of the currency to UAH 40 on the black market as of this morning. While pressures have subsided somewhat (with black-market, mid-market spot now around UAH 33), in our view, the current FX controls are only likely to provide temporary relief to the currency and, thus, introduce risks that the authorities could tighten FX controls further. Given that capital flight, debt repayments, ongoing imports and a destabilization of expectations in the FX market are likely to continue exerting pressure on the Hryvnia in the coming days and weeks, our base case of IMF fund disbursement in mid-March may not come quickly enough to stabilize the Hryvnia. In our view, this could cause the authorities to resort to more severe FX controls and/or could cause international donors aware of the fragility of the situation to make available emergency funds in order to serve as a bridge until IMF loans arrive.

Authorities step up FX controls, as pressure builds on Hryvnia …

The Ukrainian authorities have put in place an array of FX controls since late 2012, including the mandatory sale of FX proceeds, bank FX withdrawal limits, FX bank transfer limits, and de facto restrictions on access to NBU FX provision for banks. The latter restriction caused the black-market Hryvnia rate to be 20-30% weaker than the official rate in recent months, but was dismantled in early February, leading to a sharp depreciation of the Hryvnia and aligning the official exchange rate to the black-market one. Despite these restrictions, the Hryvnia continued to weaken last week, with the official rate reaching UAH 27.9 vs. the USD as of February 20 and the black-market rate rising to UAH 31 over the weekend.

As a result, in the past week, the authorities have stepped up their FX controls significantly. The government discussed imposing a duty on non-essential imports last week and the NBU earlier this week increased scrutiny and put into place checks on import pre-payments exceeding US$50,000 (and required a letter of credit from an investment-grade-rated bank for those exceeding US$500,000), while also banning leveraged FX purchases by corporates. The Hryvnia continued to weaken in response to these measures, to UAH 35 vs. the USD yesterday on the black market, and the NBU accordingly introduced further restrictions, including a complete ban on corporate purchases of FX through end-week and restrictions for banks as well. The initial response to these measures was a sharp weakening of the Hryvnia on the black market to in excess of UAH 40 vs. the USD this morning, but the end-day rate has now settled down to around UAH 33, although the bid-ask spread has widened sharply to about 15% of the mid-market price, indicative of very poor liquidity conditions. While the official rate had been aligned with the black market during the period February 6-21, it has returned to being about 20% stronger than the black market in the past several days.

There are several causes for the weakening of the Hryvnia:

- Net private capital outflows (excluding net IMF/official sector flows), which stood at an estimated US$10bn in 2014. This number excludes US$3.7bn in repayments to the IMF and about US$4.5bn in debt service on external sovereign bonds.

- Current account and trade deficits, due to the collapse in exports and despite the fact that domestic demand has weakened sharply.

- Monetary financing of Ukraine’s fiscal deficits.

While Ukraine’s current account and trade balances should close as domestic demand continues to contract and as the Hryvnia has weakened further, capital flight continues, with bank FX deposit outflows of US$600-700mn/month in November-January. Moreover, monetization of the deficit has accelerated as local banks are no longer able to absorb domestic bond issuance. The share of domestic government bonds owned by the NBU has risen to 71% in January, from 59% one year prior, with the share held by domestic banks falling by the same amount (to 20%). Meanwhile, narrow money continues to grow at around 15-20%yoy, at a time when domestic credit is now contracting by 10%yoy. While money supply growth in the mid-single digits in a context of weak credit growth may have been offset for most of 2014 by large-scale FX interventions by the NBU, withdrawing liquidity, FX interventions have slowed in H2-2014 and the NBU reportedly stopped intervening in February (although it intervened once again by US$80mn today). This has caused assets on the NBU’s balance sheet to grow by about 60%yoy in recent months and by 8%mom in January (seasonally-adjusted). In our view, with the economy and cash demand weakening, domestic credit shrinking and an absence of liquidity withdrawal via interventions, money supply growth at the current pace will ultimately prove inflationary and will cause the Hryvnia to weaken further.

While monetary financing of the deficit may debase the value of the Hryvnia in the medium term, it is the shortage of FX in the system that has caused the proximate pressure on the currency, as NBU reserves declined to US$6.4bn in January (4 weeks of imports) and are likely to decline to US$5-5.5bn in February (3 weeks of import cover). These international reserves include about US$1bn in monetary gold, so the liquid amount of reserves is likely to fall to US$4-4.5bn in February (2.5 weeks of imports).

… raising short-term risks, until IMF funds arrive …

In our view, while the current FX controls may provide some temporary relief, pressure is likely to continue to build on the Hryvnia until expectations stabilize, confidence is restored, and the country’s FX reserves are replenished. Given the poor liquidity and destabilization of expectations in the FX market, the ongoing conflict in Donbass that undermines confidence, and the continued need to import natural gas and other essential goods and make external debt payments, these factors are likely to continue to exert pressure on the Hryvnia, at least until the IMF Board approves the newly-agreed program and makes its first disbursement. However, this will likely take at a minimum 2-3 weeks and there are risks of delays. First, the authorities must fulfil their prior actions for the program, and notably the Rada must approve a new budget law. This is scheduled to take place in a session on March 3, although PM Yatseniuk is attempting to accelerate this process by holding an extraordinary Rada session to approve the legislation. Even if the session is moved forward, in our view, there is no guarantee that the law will be approved immediately and delays are possible. Once prior actions are fulfilled, the IMF Board can meet, approve the new program, then disburse funds shortly thereafter. Our base case is that this will take place in mid-March (the current board review date is reportedly scheduled for March 11), although it is possible that this could be delayed. With the current pace of reserve depletion and pressure build-up on the Hryvnia, it is possible that the IMF funds may not arrive quickly enough. This raises the short-term risk of a significant further increase in pressure on the Hryvnia.

… and implying potential need for emergency policy action

Given the balance of payments and monetary pressures on the currency, the authorities and international donors, in our view, have several policy options. First, the Ukrainian authorities could tighten FX controls further. In the extreme, this could potentially involve a bank deposit freeze, a ban on retail FX purchases and/or moratorium on external payments and complete closure of the capital account. Second, international donors (bilateral lenders and IFIs) could recognize the fragility of the current situation and the fact that the IMF timeframe may prove to be too slow to stabilize the currency. Thus, in our view, the international community could make available emergency funds in the coming days or weeks, effectively bridging financing for Ukraine until the IMF disbursement arrives. However, bureaucratic, legal and political hurdles may exist to any large-scale emergency disbursement to Ukraine, either bilaterally or multilaterally. Thus, there is no guarantee that such emergency funds could or would be made available. This introduces further short-term policy uncertainties.

Finally, the recent and sharp weakening of the Hryvnia, as well as significant recent shifts in money demand and supply, could necessitate an overhaul of some of the IMF’s program assumptions and targets. In our view, this could require further technical work on the part of the IMF and could cause additional delays to disbursement of IMF funds. As the monetary and financial dynamics evolve rapidly, so may the IMF’s working program assumptions and the parameters of the program.